More Singaporeans dealing with rising mortgage stress: Survey

PHOTO: Pexels

In its annual financial wellness survey, OCBC Bank uncovered a trend of rising financial stress amongst Singaporeans. One of the key drivers for this increase in financial stress comes from their mortgage, which is driven by the rising interest rate environment as the US Federal Reserve continues to raise interest rates to fight inflation.

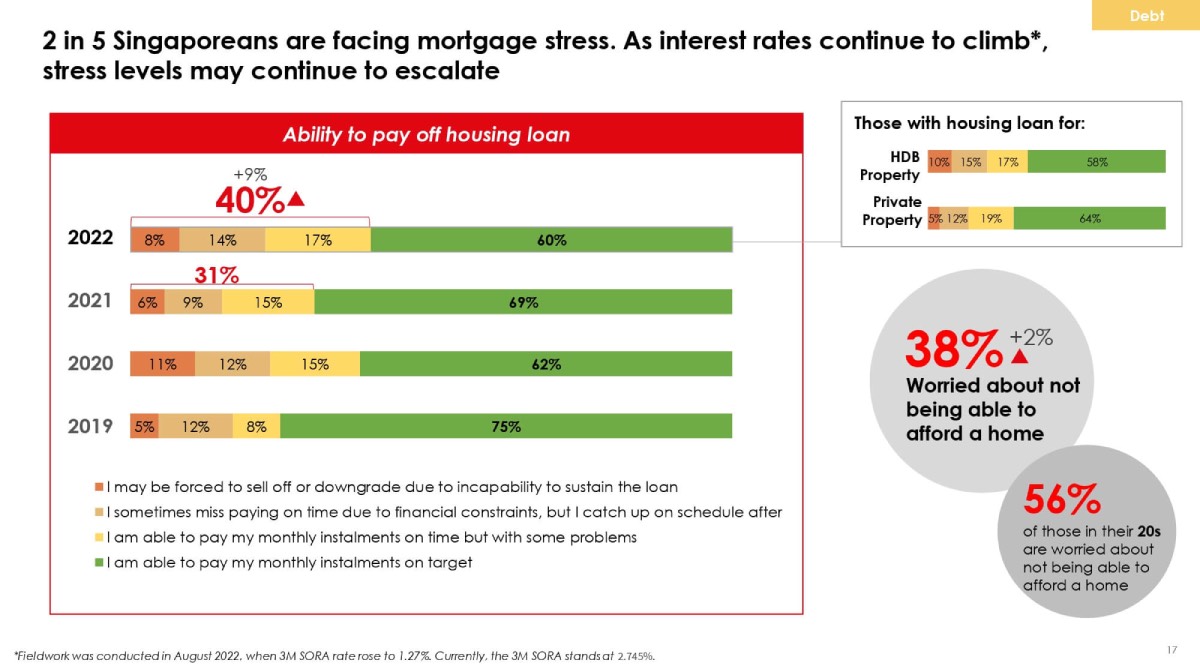

According to the OCBC Financial Wellness Survey, 40 per cent of Singaporeans are facing mortgage stress due to rising interest rates. This was up from 31 per cent in 2021 and seems to be on a rising trend across the four years the Survey has been conducted.

One worrying sign is that the percentage of Singaporeans who feel that they are not able to pay off their monthly instalment is the highest it has been for the last four years. The figure is even higher than 2020, when the economy was reeling in from the initial impact of the Covid-19 pandemic and economic shutdowns.

That said, there might be the smallest of silver linings. For instance, the percentage of Singaporeans who feel that they may be forced to sell off or downgrade because of inability to service the mortgage makes up only eight per cent. This is a lower proportion than in 2020 (11 per cent).

The hard truth is that mortgage stress might be much higher now than it was during the time this survey was completed. At the point of the survey, the 3M Singapore Overnight Rate Average (SORA) was 1.27 per cent. The 3M SORA is currently standing at 3.69n per cent at the time of writing (Sept 8, 2023). That's a whopping 2.90x of what it was just a year ago.

For any homeowner who has an existing mortgage to finance, it is important that you take some time to review your existing bank loan package. Make some comparisons against the latest bank loan deals in the market to see if you can eke out any savings. Any savings you can find will help you to better manage your mortgage stress.

If you need help, you can consider engaging a mortgage consultant. Mortgage consultants can help you with your refinancing and relieve you of the financial stress.

Some say that the era of cheap financing has ended. Singaporeans are starting to feel the pinch of financing big ticket purchases like housing. This problem is further exacerbated by the fact that a labour crunch has led to housing demand outstripping supply, causing homes to rise to a historical record in 2022. It is no wonder why 38 per cent of Singaporeans are worried about not being able to afford a home.

And when we analyse the situation among younger Singaporeans, 56 per cent of Singaporeans in their 20s are worried about housing affordability. Indeed, owning a home now in your 20s is a far cry away from our parents' generation.

One tip that we can offer aspiring homeowners is to take your mortgage seriously. Review it every couple of years once the lock-in period is over so that you are always on the best deal possible. Every dollar you can save from unnecessary interest payment is a dollar that you can channel into the actual value of your home.

Another stark reminder from the survey findings is the contrast of plight between HDB and private property owners. HDB owners seem to be in a much better financial shape as compared to private property owners.

One possible reason for this is because many HDB owners are under the HDB housing loan. Despite the rising interest rate, most HDB owners are still sticking to the same interest rate (CPF OA + 0.1 per cent) when they first signed up for the mortgage.

Unlike HDB owners, private property owners are feeling the impact of rising interest rates more. Many, if not all, private property owners have seen their mortgage interest rate go up in recent years. In Singapore, home loans from banks and financial institutions don't stay fixed forever. Most private home owners will eventually find themselves on a floating interest rate package. And while that was the best deal in the past few years, it's definitely no longer the case.

ALSO READ: 3 strategies to manage your monthly bank loan repayment

This article was first published in Mortgage Master.