Why are private home sales and HDB prices rising despite the recession?

PHOTO: Stackedhomes

From all the property news you’ve read, you might be inclined to think real estate is pandemic proof.

As of August, new private home sales in Singapore are up for a fourth straight month – according to URA data, 1,307 new non-landed private homes (including Executive Condominiums) were sold, up about 16.3 per cent from July.

[embed]https://www.facebook.com/TheStraitsTimes/posts/10157364728957115[/embed]

On the HDB front, resale HDB prices seem to be on the rise after almost seven years of decline.

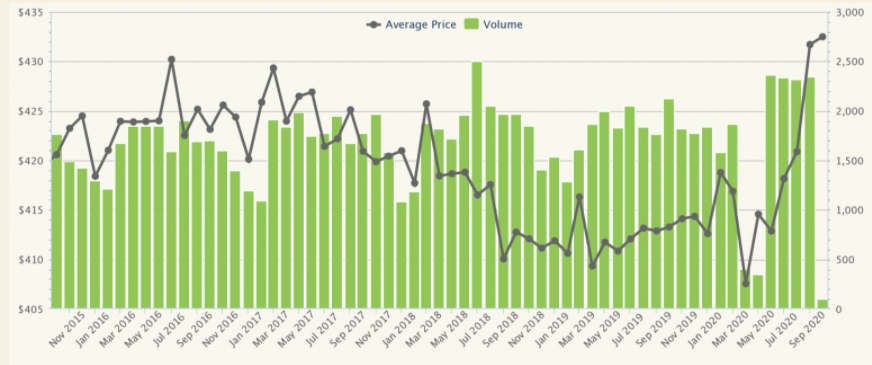

Resale HDB prices are up 1.4 per cent in Q3 2020, with momentum gaining after a 0.3 per cent increase in Q2. Perhaps a graph will best demonstrate how dramatic the price movement has been:

If we look back five years ago, resale HDB prices (average for all flat types in all towns) were $421 psf. April saw it fall to the lowest point in five years, at $408 psf.

By August, the price had rocketed back up to $421 psf, the same as five years previous; and by September prices were up to $432 psf, and rising.

This is an increase of 5.8 per cent since April; and what stands out is that the sharp increases happened during the circuit breaker months, at the height of the Covid-19 outbreak.

While it’s too early to say for sure, here are some of the common reasons from analysts and agents. Do note that some of these don’t fully agree with one another, and more time is needed for a clearer picture:

In an earlier article, we mentioned that URA has restricted the re-issuing of the Option To Purchase (OTP).

This is related to the issue of inflated sales numbers in new launch properties. We also pointed out how bad the distortion can get, when in 2018 around two-thirds of the reported sales were “returned”.

In other words, many of the supposed “sales” we’ve seen in the past quarter may not be real – they may simply reflect the number of Options issued, many of which may not be exercised after all.

This means sales figures are simply inflated, disguising the impact of the downturn.

The only way to know is to wait, and see the figures for Q4. If it’s true that many of the transactions were just a façade, caused by re-issued OTPs, we may see a notable drop in sales volume the coming quarter.

(It’s fair to also note, however, that the restrictions may also impede certain groups of buyers – such as upgraders who need more time to sell their previous home, or those who face financing delays.

This could drive down sales volumes for the coming quarter, so we may have also caused lower transactions, in the pursuit of clarity).

Bank loans (which can be used for both private and HDB properties) are at a historical low. This is due to the United States’ Coronavirus response, in which the Federal Reserve has committed to a near-zero interest rate till at least 2022.

The current 3M SIBOR rate, to which many home loans are pegged, is 0.41 per cent at the time of writing. For comparison, the rate was 1.77 per cent in January this year.

The corresponding effect is that bank home loans can now be had at rates of 1.2 to 1.3 per cent per annum; about half the HDB loan rate of 2.6 per cent.

As an example of the cost difference, consider a loan for $1 million at two per cent (common in 2018), for 25 years. This would result in monthly payments of $4,239 per month, with total repayments of about $271,560 by the end of the loan tenure.

Reduced to 1.2 per cent, monthly repayments fall to $3,860 per month, with total repayments amounting to about $158,000 by the end of the loan.

(For readers who are currently facing much higher rates than 1.2 or 1.3 per cent, contact us on Facebook; we may be able to help you refinance into a cheaper option).

The lower home loan repayments may be enticing to buyers, as they’re even lower than our guaranteed CPF interest rate (2.5 per cent).

Covid-19 has caused delays in the construction industry, which could impact the completion dates of HDB flats. Singaporeans who want a home quicker may now be inclined to choose already completed resale flats, thus sparing them a longer wait.

On top of the logistical reasons, we should remember that the Minimum Occupation Period (MOP) of five years starts from the date of key collection.

So if you intend to upgrade from an HDB to a condo, you would wait at least five years with a resale flat.

But if you pick a BTO flat, you would wait three to five years for construction to be finished, and then start counting down another five years for the MOP.

This makes any delay in the construction process much more painful, as private home prices could be ticking up for every quarter you’re waiting.

This would bode well for resale flat demand in general.

There are twice as much available in grants for resale flats (up to $160,000), than there are for BTO flats (up to $80,000).

Resale flat buyers can get the Family Grant (up to $50,000 for a four-room or smaller flat, and $40,000 for larger flats); they also have a shot at the Proximity Housing Grant for living near their parents, which is up to $20,000.

On top of this, we may be seeing price support for resale flats, which commenced in May 2019. At the time, CPF rules were changed, allowing you to tap CPF monies even for flats with just 20 years left on the lease.

HDB also removed the old “60-year-limit”; this allows you the full 90 per cent financing on a flat, so long as the lease can last till you’re 95 (and there’s at least 20 years remaining).

The more generous grants and CPF usage rules, coupled with a need for prudence, could see some buyers turn from even private properties and ECs to resale.

It may have just taken a while for the changes in 2019 to sink in, and the Covid-19 situation may have helped to accelerate it.

For foreign investors, Singapore real estate has been seen as a safe haven for some time; Marina One Residences even sold some $20 million worth of units to Chinese investors, sight unseen, during the Circuit Breaker.

But foreigners aside, Singaporeans may see it the same way. During the last Global Financial Crisis in 2008/9, for instance, real estate prices bottomed out in around February 2009 (non-landed).

It took only 14 months for real estate prices to recover. Between 2009 and 2013 (the last property peak), home prices were up 60 per cent across the board; and the prices only came down following a slew of cooling measures in 2014 onward.

As such, some investors may simply trust what they’ve seen in the past; the downturn could incentivise, rather than discourage, higher numbers of private property transactions.

Right now, it’s hard to read the situation as Covid-19 is unprecedented, and we’re in the middle of it. However, Q4 could reveal much that’s interesting about Singapore’s real estate scene.

For starters, we should have a clearer idea whether property sales have been inflated in the past, due to the re-issue of OTPs.

Second, we’ll see if the long night of declining resale flat prices has finally come to an end; and if resale flat prices have any hope of returning to the property heyday of 2013.

This could change the prevailing market view, which in past years have looked more cynically on resale flats as “retirement gold.”

This article was first published in Stackedhomes.