HDB resale grants: How much can you get? (2023)

PHOTO: Pexels

Buying an HDB resale flat comes with its perks - one of it being the generous HDB resale grants you can qualify for.

In 2019, HDB raised the income ceiling for the CPF Family Grant from $12,000 to $14,000 and launched the new Enhanced CPF Housing Grant (EHG). This enables more resale buyers to qualify for housing grants and get a higher maximum grant amount of up to $160,000.

Around four years later in 2023, in a bid to make HDB resale flats more affordable for first-timer families and singles, HDB increased the Family Grant and Singles Grant amounts.

| Flat type | Previous grant amount | Current grant amount | |

| Family Grant | Two to four room | $50,000 | $80,000 |

| Five room or larger | $40,000 | $50,000 | |

| Singles Grant | Two to four room | $25,000 | $40,000 |

| Five room or larger | $20,000 | $25,000 |

These changes could mean that HDB resale flats may turn out to be cheaper than a Build-to-Order (BTO) flat after all, even though BTO flats are sold by HDB at a discount. After all, the Family Grant and Proximity Housing Grant are not applicable for BTO flats.

Plus, the key perks of buying a resale flat are an unlimited choice of locations and the fact that resale flats are already completed and ready for moving in. Resale flats also typically have well-developed amenities, such as schools and eateries, surrounding them.

Now, it's time to know your HDB resale grants. This article will cover:

And we've created a chart to help you determine the grant amount you'll get as well, if you're a first-timer. Scroll down to see it.

Get ready, it's quite a long list. (There's a handy infographic below, too.)

To be considered a first-timer applicant, you must:

How much:

Income ceiling:

To qualify for the Family Grant, the buyers' household income must not exceed $14,000. The exception is when applying to live with extended families; for this, the income ceiling is $21,000.

The higher grant amount is to encourage older couples or working adults to live with their extended families - including siblings and parents.

Note: The income ceiling for this and other grants is calculated by taking the monthly average of your total household income for the past 12 months, calculated up to two months before the HFE letter application (more on this later).

Who can qualify for the Family Grant:

If one party is a Singapore Permanent Resident (SPR), they will receive $10,000 less (i.e. $70,000 for two to four room; $40,000 for five room or larger).

Additional criteria:

How much:

Income ceiling:

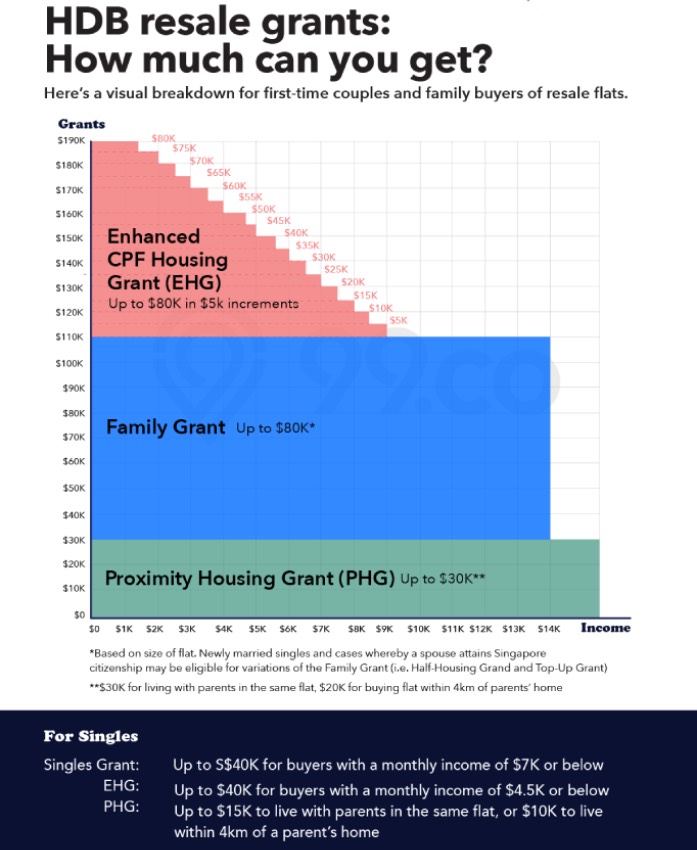

To qualify for the Enhanced CPF Housing Grant (EHG), the buyers' household income must not exceed $9,000. This is also a tiered grant, meaning that the lower your income, the higher the EHG amount you may be eligible for.

(To know how much in EHG you can get for a specific household income, see the infographic below.)

You can qualify for the EHG if you meet all of the following criteria:

Additional criteria:

How much:

Income ceiling:

Good news, the PHG has no income ceiling restrictions!

Additional criteria:

You can use the infographic to find out, at a glance, how much HDB resale grants you may be eligible for. Here's an example:

Let's say you and your spouse are first-time applicants, and would like to buy a five room HDB resale flat near your parents' home. With one child and a baby on the way, living near your parents will give you peace of mind. You will receive:

You are earning $5,000/month, and your spouse is earning $3,500/month. The average gross monthly household income is $8,500. This means:

In this scenario, you're eligible for a total of $80,000 in HDB resale grants. Not bad!

First of all, you need to be aged 35 and above to buy an HDB flat as a single.

How much:

*Singles applying under the Single Singapore Citizen Scheme will not qualify for the Singles Grant if the flat size exceeds a five room flat (e.g. an executive flat).

Income ceiling:

To qualify for the Singles Grant, your average household income for the past 12 months (calculated up to two months before the HFE letter application) must not exceed $7,000 if you're buying under the Single Singapore Citizen Scheme.

If you're buying with family members or other singles with the Joint Singles Scheme, the income ceiling is $14,000.

Additional criteria:

How much:

Income ceiling:

To qualify for the Enhanced CPF Housing Grant (EHG) for Singles, the buyer's household income must not exceed $4,500. This is also a tiered grant; the lower your income, the higher the EHG amount you may be eligible for.

You can qualify for the EHG for Singles if you meet all of the following criteria:

Additional criteria:

How much:

Income ceiling:

Good news, the PHG has no income ceiling restrictions!

Additional criteria:

Previously received a grant as a single but got married? HDB lets you top up your grant!

How much:

Income ceiling:

The combined income of the household must not be more than $14,000 a month, based on the average income for the past 12 months*.

You can qualify for the Top-Up Grant if you meet the following criteria:

Here are HDB's full terms and conditions for the Top-Up Grant.

For Singapore citizen/ Singapore Permanent Resident (SC/SPR) households with a household member obtaining Singapore citizenship status, they are eligible for a Citizen Top-Up Grant of $10,000.

This household member can either be:

There are no maximum household income restrictions, although you'll need to submit your application within six months of getting your Singapore citizenship.

Yes, there are grants for you too.

How much:

Income ceiling:

The combined income of the household must not be more than $7,000 a month, based on the average income for the past 12 months, calculated up to two months before the HFE letter application.

For who?

Here are the full terms and conditions.

How much:

Income ceiling:

The combined income of the household must not be more than S$14,000 a month, based on the average income for the past 12 months, calculated up to two months before the HFE letter application.

For who?

Previously called the Half-Housing Grant, the amount for this grant is basically half the amount of the Family Grant for first-timers. It's reserved for first-time applicants whose spouse/fiance/fiancee has previously received a housing subsidy.

Like the Family Grant, the average monthly income should not exceed $14,000 or, for those applying to live with extended families, $21,000.

Here are the full terms and conditions.

With the three main grants - Family Grant, EHG and PHG - available for resale flats, you may be eligible to receive a total of $190,000. Pretty impressive, huh?

In comparison, the typical BTO applicants will be eligible for a total maximum of $80,000 in grants, as they may only be eligible for the EHG. BTO applicants do not qualify for the Family Grant or the Proximity Housing Grant.

And if you are wondering why the large gap, it is because resale flats are generally sold at market value. On the other hand, BTO flats are sold by HDB at a discounted amount. The discount is mainly due to the additional waiting time involved for a BTO flat to be built.

For certain locations and towns, if you factor in the higher HDB grants available for a resale flat, the cost of buying an HDB resale flat can be even lower than a BTO flat.

(Of course, the catch is that the cheaper HDB resale flat may have a lower remaining lease, whereas a BTO flat comes with a fresh 99-year lease.)

You'll need to apply for the HFE letter before the owner issues you an option to purchase (OTP) a resale flat.

Based on certain criteria such as income, HDB will determine your eligibility to

One thing to note is that the income assessment period is 12 months, calculated up to two months before the HFE letter application. This may affect your eligibility to get certain grants that have an income ceiling.

Moreover, the HFE letter will be processed within 21 working days. So you may want to apply for the HFE letter before starting your home-hunting journey to get a better picture of how much you can afford.

After you've received the HFE letter, you can proceed with searching for your dream home.

Once you and the sellers have agreed on the asking price, and have exercised the OTP, you will then need to submit a resale application via the HDB Resale Portal (your agent may assist you on this).

On your resale application, you'll be asked to specify which housing grants you are applying for.

Once approved, the housing grants are disbursed to your CPF Ordinary Account (CPF OA) to pay for your HDB resale flat upfront. The grant amount is first used to cover any outstanding downpayment of the flat, before being used to reduce the amount you need to loan.

But here's the catch. When you eventually sell the flat you received these grants for, you will need to return them, as well as a 2.5 per cent per annum interest for every year you've had your flat, back to your CPF OA. The good news is that you can use it for your next home purchase.

ALSO READ: What is the HDB Resale Price Index? 2023 guide for homeowners (to-be) in Singapore